Who Makes Money from Agents?

A lot of people theorize that agents will be the next billion blockchain users. Few have asked the second-order question: in that world, who makes money?

Every prior value capture thesis in crypto has assumed the user is a human. Fat Protocols said protocols would be best at monetizing them. The Fat App thesis my colleagues and I have written about in How to Capture Value and The Great Repricing argues apps do it better. Agents change who the user is, and the existing theses stop being reliable.

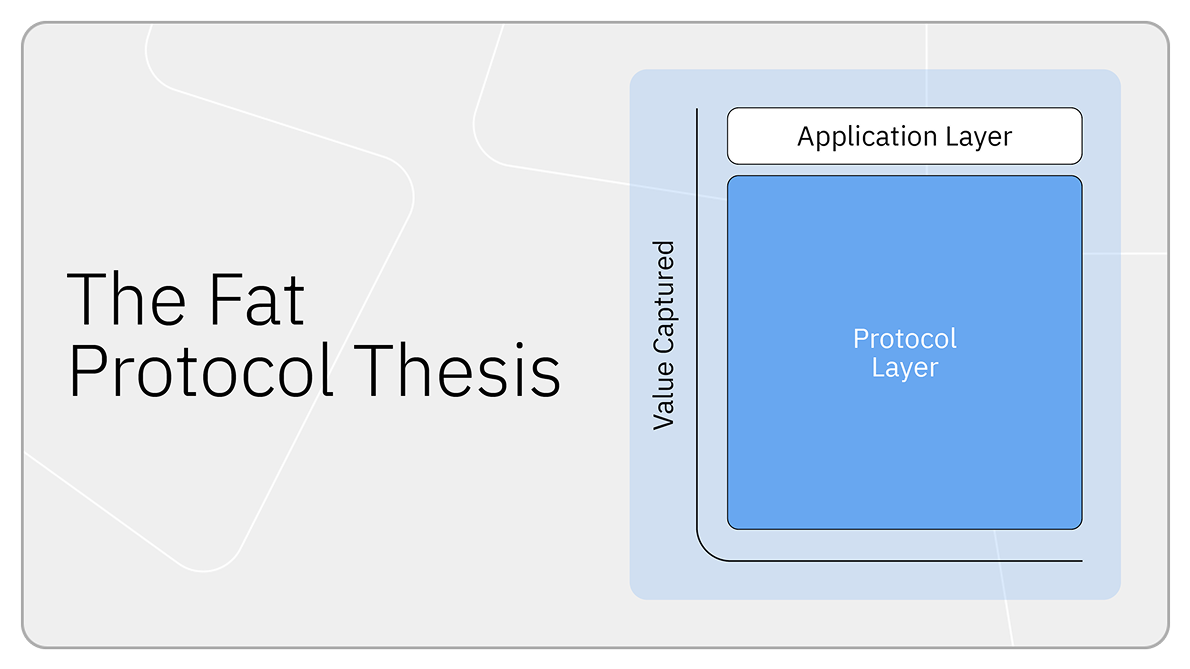

The Fat Protocol Thesis

In 2016, Joel Monegro wrote Fat Protocols. It became the dominant value capture thesis in crypto for the better part of a decade. The argument: on the internet, value accrued to applications (Google, Facebook) while the underlying protocols (TCP/IP, HTTP) captured almost none. Crypto would flip this. Blockchains share data openly, so apps would get commoditized. The protocol's token, required to use the network, would capture the speculative value of usage as it grew. Every app success would drive token demand. The protocol would compound faster than anything on top.

For years, this looked right. Bitcoin and Ethereum were worth more than any company built on them. The model worked when the protocol was scarce, expensive to build, and hard to substitute. Bitcoin and Ethereum genuinely were scarce in 2017 and there weren't a dozen general-purpose L1s competing for the same workloads. Blockspace was constrained enough that holding the underlying asset felt like holding a piece of every app that needed it.

Now there are credible alternatives at every layer of the infra stack: multiple high-throughput L1s, dozens of L2s, modular settlement and DA layers competing on price. Blockspace went from constrained to abundant. Switching costs collapsed as bridges and aggregators made the underlying chain almost invisible to users. Infrastructure became interchangeable, and interchangeable things compete on price. As a result, protocols' pricing power went with the scarcity.

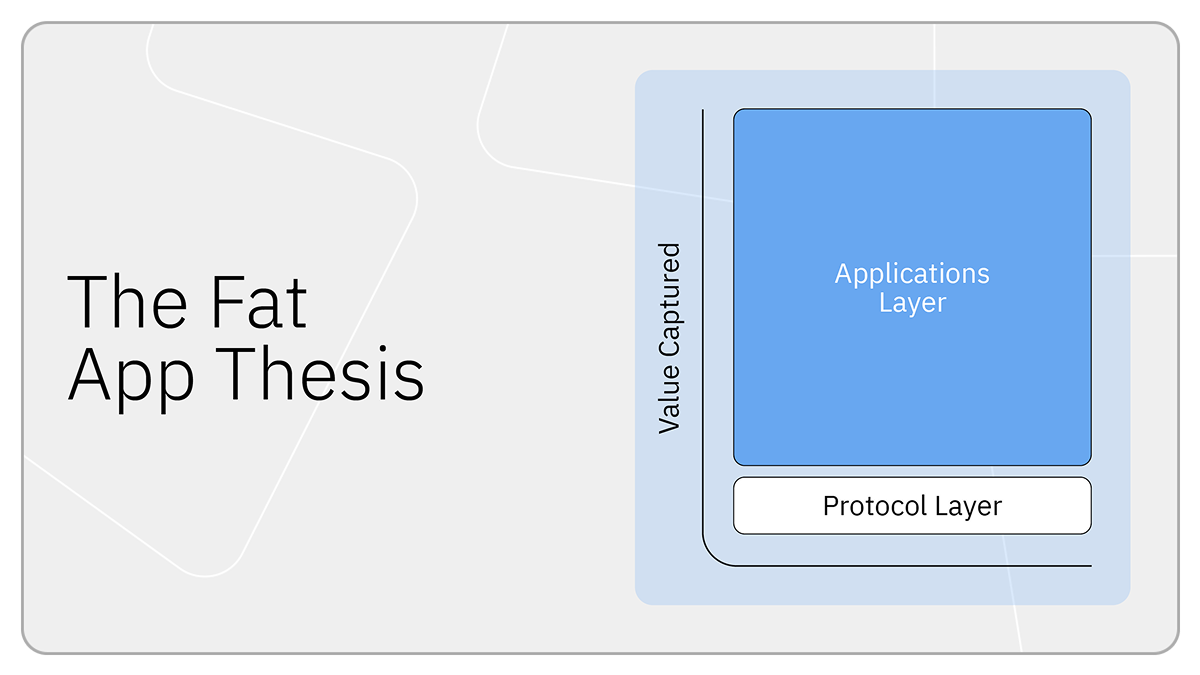

The Fat App Thesis

The entities capturing much of the economics in 2026 are the apps, not the protocols: Phantom, Coinbase, Polymarket, Pumpfun, etc. The reason, imo, is that the most valuable asset in crypto is the user relationship. If you control the user interface and the flow of transactions, you control distribution, and you can monetize nearly any onchain product your users touch: swaps, lending, staking, mints, ramps. This is probably why funds are so obsessed with neobanks.

Apps also push infrastructure into pure price competition, which compresses infra margins toward marginal cost. I document this strategy in How to Capture Value. The same dynamic is playing out in stablecoins, which I cover here.

Prices are reflecting this thesis. Spencer and I called this shift The Great Repricing: in this cycle, value accrued to the layer that owned the user.

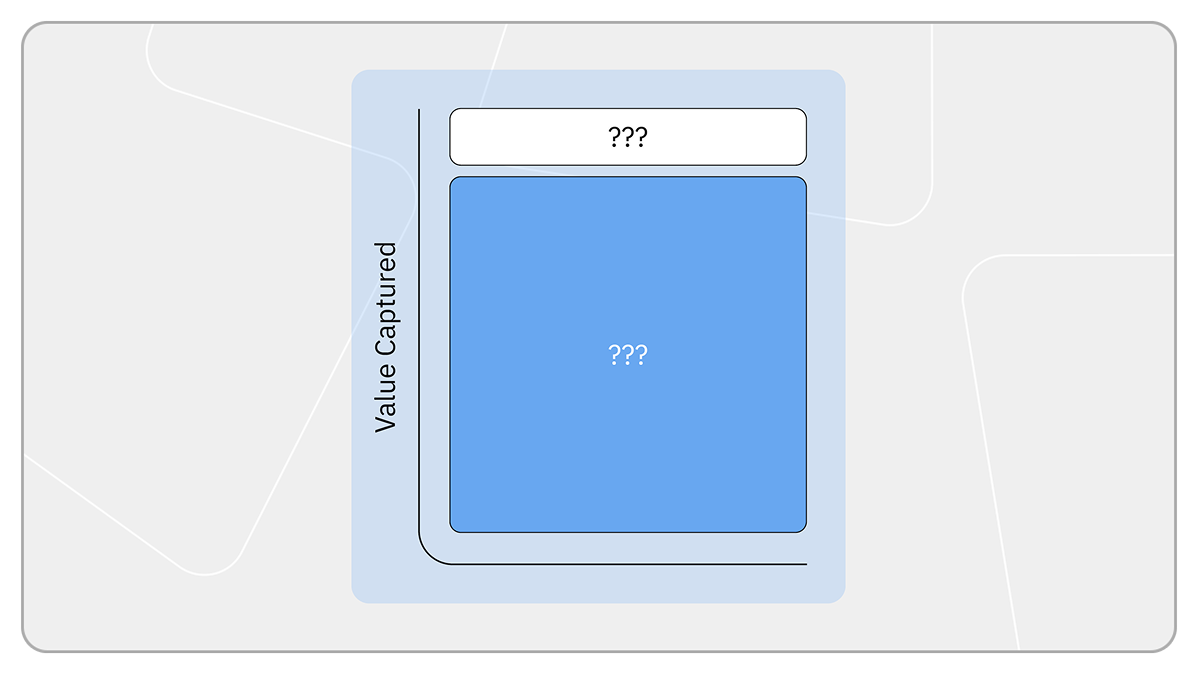

Why Agents Break This

The Fat App thesis assumes the user is a human who values UX, brand, and convenience. Agents value none of those. They go directly to APIs, have no brand loyalty, and switch venues at zero cost. When the user is software, owning the user relationship stops being defensible. The frontend moat the entire Fat App thesis rests on depreciates.

So who captures value in the age of agents?

The Apps Go Headless

In one version of the future, app-layer winners stay winners by shedding the UI. Wallets and aggregators have already built the hard parts: the integrations with dozens of protocols, the routing logic, the identity and ramp infrastructure. The natural next move is to expose that stack as an agent-facing API and let agents route through them the same way humans route through Phantom or Jupiter today. In this world, the Fat App thesis survives. It just loses the frontend. The companies that won the human era re-platform as headless infrastructure. We are already seeing traditional SaaS businesses like Salesforce going this direction.

Protocols Re-Emerge

In a different version, agents skip the middle layer entirely. If integration is easy enough (well-documented APIs, standardized RPCs, predictable execution semantics), there's no real reason for an agent to pay an aggregator to do something it can do itself. The aggregator's edge in the human era was UX and routing complexity. Agents don't need UX, and routing is a solvable engineering problem that agents are increasingly good at. If that's the world, the Fat Protocol thesis gets a second life.

Pricing Power Collapses Across The Stack

Maybe agents apply commoditization pressure everywhere. They're perfectly rational. They route to the cheapest venue every time, with no loyalty and no friction. Apps lose the premium they were charging humans for UX. Aggregators and infra lose their pricing power too, because there's no human inertia to insulate them from price competition.

In this scenario, nobody in the stack captures much. The whole supply chain compresses toward marginal cost, and the surplus accrues to whoever owns the agent or to the end user the agent is acting for. Crypto becomes a utility, and utilities are hard places to make money.

Agents Create Activity That Wasn't Viable Before

The simple version of this argument is that agents do everything humans do, just at higher throughput, and that compressed margins on much higher volume still grow the pie.

I think there's a more interesting version. Agents make a class of activity viable that wasn’t viable before (e.g., continuous portfolio rebalancing at sub-cent execution costs, machine-to-machine commerce between agents, and markets that only make sense because they’re priced and traded faster than any human could meaningfully follow). None of this shows up in the current view of onchain activity because we assume a human in the loop.

If that’s what agents bring, the question shifts from how the existing pie gets divided to how much new economic activity comes onchain, and which layers are positioned to serve it.

A Business Model That Doesn't Have a Name Yet

Every cycle, we try to guess where value will flow, and we tend to assume the business models we already know will extend into the future. That assumption usually misses the models that don't exist yet.

Nobody predicted the attention economy when the internet was being built. The idea that the dominant business model would be auctioning slices of user attention to advertisers, and that a single company would extract a meaningful share of global ad spend from it, was foreign. It only looked inevitable in hindsight.

AI looks like one of the biggest technology disruptions in decades. Some of the value capture in an agentic world will probably accrue to a business model nobody is writing about today. The parties that capture it may not be the ones the market is watching.

What to Watch

The most likely outcome isn't one regime replacing another. Humans and agents will coexist as the users of crypto for a long time, and the value capture map for each looks different. The Fat App thesis still applies wherever humans touch the chain: consumers who pay for UX, brand, and convenience will keep paying premiums to the apps that own that relationship. A separate thesis, whichever of the scenarios above plays out, will govern the surface where agents transact.

For builders, imo, the question worth obsessing over on the agent side is what makes an agent come back to you instead of routing to the next cheapest alternative. UX might not be the answer. Liquidity, latency, settlement guarantees etc. might be.

At BCAP we're spending a lot of time on this question, both in investment committee meetings and with our engineering team. We don't have a settled answer. If you’re building around agents and have a view on agent value capture that we should hear, we want to talk.

The content provided herein may include information regarding past and/or present portfolio companies or investments managed by Blockchain Capital or its affiliates and are provided for illustrative purposes only. The views expressed in each blog post are the personal views of each author and do not necessarily reflect the views of Blockchain Capital and its affiliates. Neither Blockchain Capital nor the author guarantees the accuracy, adequacy or completeness of information provided in each blog post. No representation or warranty, express or implied, is made or given by or on behalf of Blockchain Capital, the author or any other person as to the accuracy and completeness or fairness of the information contained in any blog post and no responsibility or liability is accepted for any such information. Nothing contained in each blog post constitutes investment, regulatory, legal, compliance or tax or other advice nor is it to be relied on in making an investment decision. Blog posts should not be viewed as current or past recommendations or solicitations of an offer to buy or sell any securities or to adopt any investment strategy. The blog posts may contain projections or other forward-looking statements, which are based on beliefs, assumptions and expectations that may change as a result of many possible events or factors. If a change occurs, actual results may vary materially from those expressed in the forward-looking statements. All forward-looking statements speak only as of the date such statements are made, and neither Blockchain Capital nor the author assumes any duty to update such statements except as required by law. To the extent that any documents, presentations or other materials produced, published or otherwise distributed by Blockchain Capital are referenced in any blog post, such materials should be read with careful attention to any disclaimers provided therein.

.png)

.png)

.png)

.png)

No Results Found.