.png)

The Price of Stability

A stablecoin is a digital dollar pegged 1:1 to fiat currency. Unlike Bitcoin, its value doesn’t fluctuate. Unlike a bank transfer, it can move instantly, anywhere, at near-zero cost.

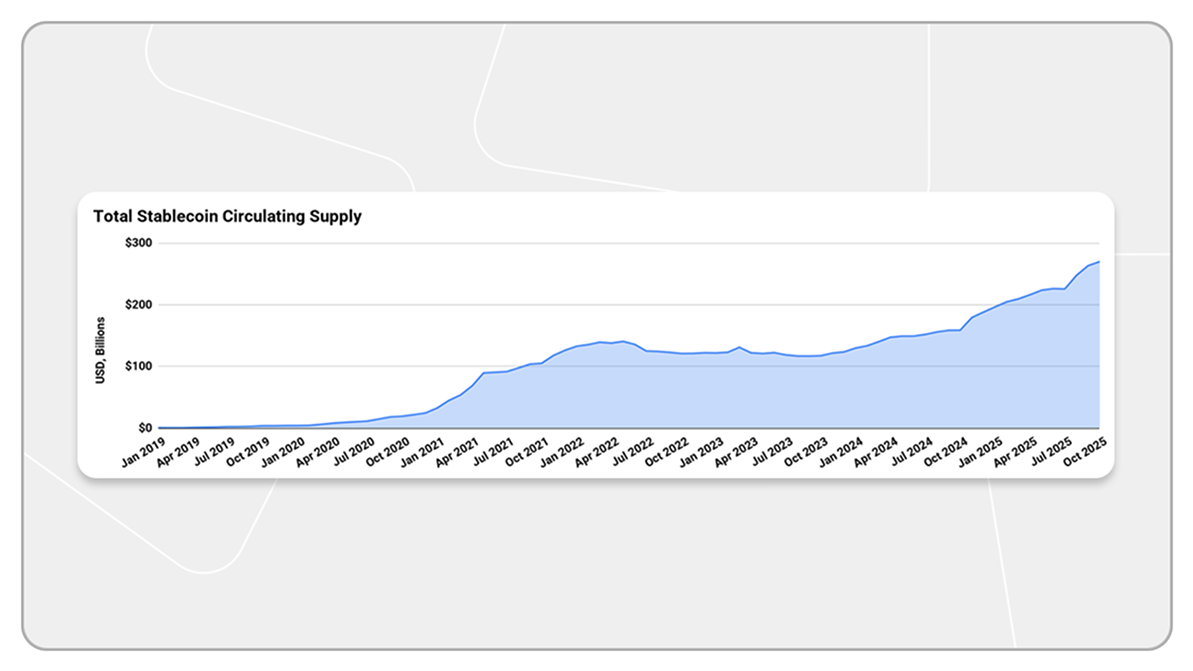

Few financial instruments have scaled this quickly. From a $1B market cap in 2017, stablecoins now exceed $300B with over $1T in average monthly volumes.

Today stablecoins have three primary uses: trading, payments, and savings.

In the first, they serve as the unit of exchange onchain, what you spend to buy Bitcoin. For cross-border payments, they are faster and cheaper than correspondent banking, especially in corridors underserved by traditional financial infrastructure. And, in high-inflation economies, they offer a flight to quality when governments debase the local currency.

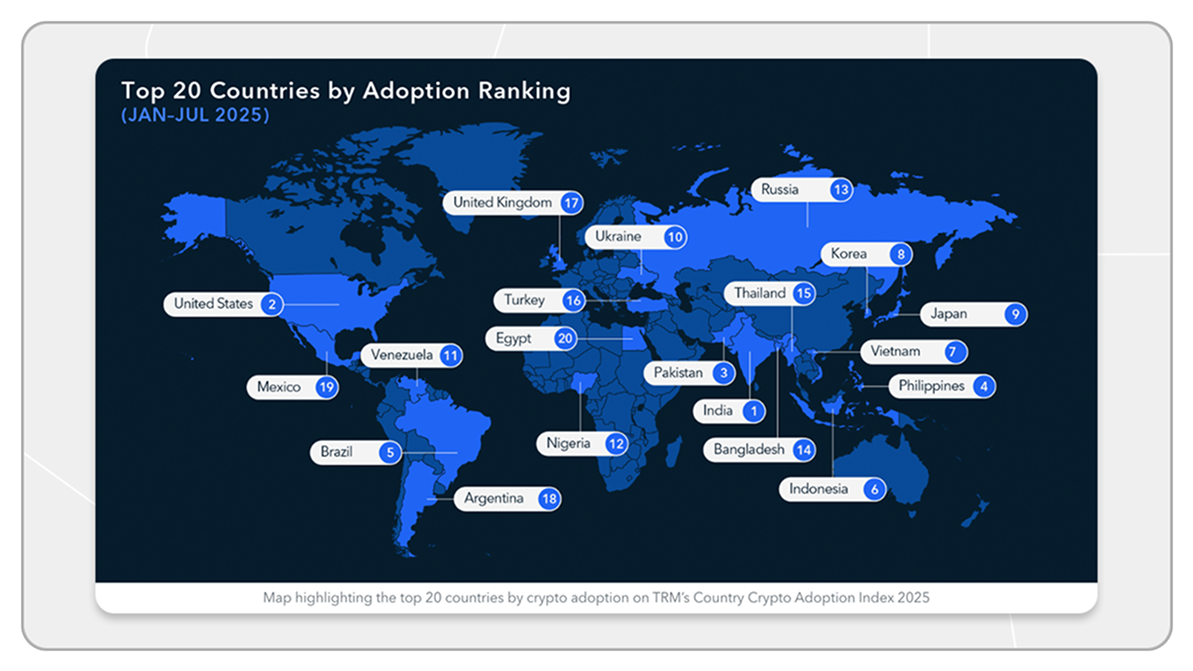

Recently, the International Monetary Fund released a study on stablecoin utilization. Their data confirmed adoption was not from traders in New York or London. Instead, growth is strongest in countries with high inflation, weak institutions, and failing monetary frameworks.

The IMF found this concerning, labeling stablecoins a potential systemic risk. The proposed remedy for governments: “maintain effectiveness of capital flow management.” In other words, close the paths for capital and citizens to exit.

But dollar demand isn’t new. Examples punctuate the historical narrative, from Weimar Germany in the 1920s to Latin America's Lost Decade, Argentina's Corralito in 2001, Lebanon in 2019, and Zimbabwe in 2008.

Historically, the wealthy opted out by moving savings offshore. Today, stablecoins provide that off-ramp to anyone with an internet connection.

The adoption patterns confirm it.

In Sub-Saharan Africa, adoption grew by 52% in the 12 months ending June 2025. Nigeria accounts for $92B in volume. When the naira devalued sharply in March 2025, volume spiked to $25B while other regions declined. Nigeria’s scale reflects not just its large, digitally native population, but specifically chronic inflation and limited access to foreign currency, both of which have driven adoption of stablecoins as a practical alternative.

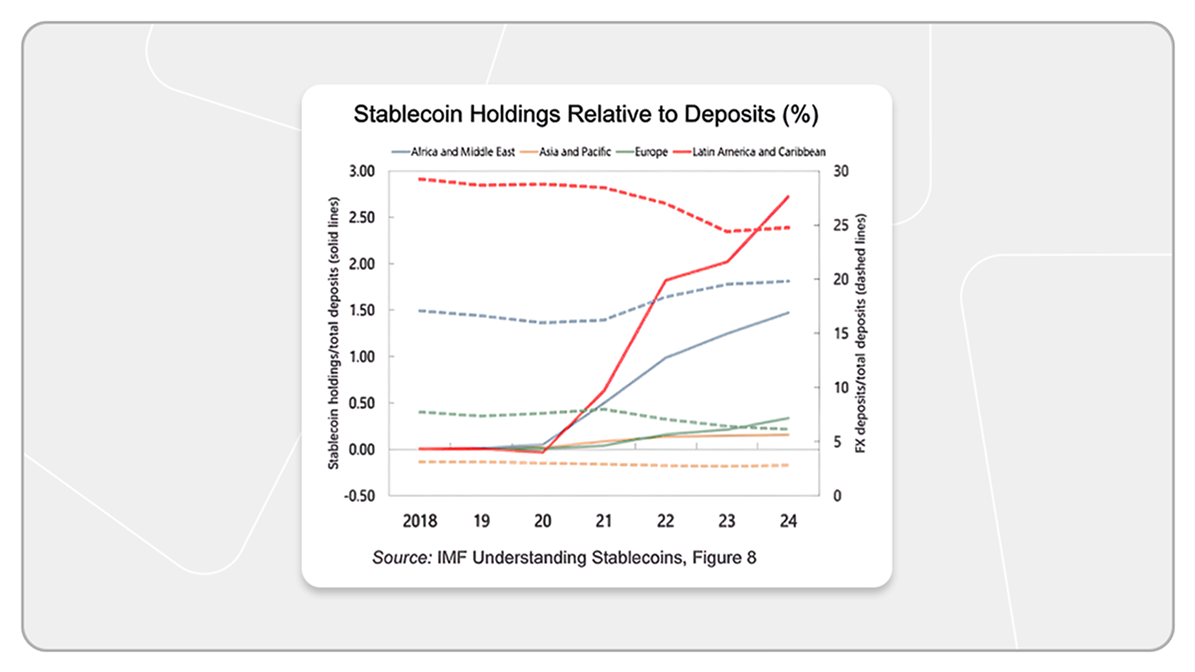

This pattern holds in Latin America as well. When the Argentinian peso lost 80% of its value and annual inflation exceeded 140%, the IMF’s own data shows that stablecoin holdings surged as traditional bank deposits began to decline.

Across APAC, remittances and cross-border payments are driving adoption. India leads, supported by fintech rails like UPI, while Pakistan and the Philippines rank #3 and #4, respectively.

Where monetary transmission is costly or institutions are weak, the structural demand for dollars emerges. Stablecoins provide all citizens with a simple way to move money and protect their savings.

Consider a typical civil servant in Nigeria earning ₦250,000 (about $150 USD) per month. Between January 2023 and March 2025, the naira depreciated from ₦460 per dollar to over ₦1,500.

Every paycheck, she faced a simple choice: leave her wages in the bank and watch her savings erode, or convert a portion into dollars via USDT and preserve her ability to afford the same life next month.

When your paycheck loses value between earning it and receiving it, the issue isn’t income. It’s preservation. From civil servants in Lagos to hospitality workers in Manila and gig workers in Karachi, stablecoins let people keep more of what they earn. These are not speculators. Instead, they are people responding rationally to monetary systems that are inefficient or failing.

When friction is removed, capital flows towards its highest utility. Stablecoins compress this friction and make a rational choice more accessible. What once required offshore bank accounts, black markets, or intermediaries under state control can now be done with a smartphone.

We accept the IMF’s contention that this compression creates real policy tension. When capital exit is a simple one-tap transaction, banking systems built on captive deposits can become destabilized. These are legitimate concerns.

But the IMF’s framework treats the exit as the problem, not the symptom.

For most of modern history, the cost of monetary failure was silently extracted from citizens through inflation and capital controls. While the wealthy opt out, everyone else absorbs the loss.

Citizens converting savings to USDT or using stablecoins to circumvent excessive correspondent banking fees are responding to a system that extracts value from the people it is supposed to serve. The wealthy have always had options. Stablecoins extend that to everyone.

That is the structural change the IMF's framework has not yet absorbed: stablecoins did not create dollar demand; they democratized access.

For the first time, the cost of bad monetary policy falls on the government that made it, not the citizens forced to hold a depreciating currency.

The content provided herein may include information regarding past and/or present portfolio companies or investments managed by Blockchain Capital or its affiliates and are provided for illustrative purposes only. The views expressed in each blog post are the personal views of each author and do not necessarily reflect the views of Blockchain Capital and its affiliates. Neither Blockchain Capital nor the author guarantees the accuracy, adequacy or completeness of information provided in each blog post. No representation or warranty, express or implied, is made or given by or on behalf of Blockchain Capital, the author or any other person as to the accuracy and completeness or fairness of the information contained in any blog post and no responsibility or liability is accepted for any such information. Nothing contained in each blog post constitutes investment, regulatory, legal, compliance or tax or other advice nor is it to be relied on in making an investment decision. Blog posts should not be viewed as current or past recommendations or solicitations of an offer to buy or sell any securities or to adopt any investment strategy. The blog posts may contain projections or other forward-looking statements, which are based on beliefs, assumptions and expectations that may change as a result of many possible events or factors. If a change occurs, actual results may vary materially from those expressed in the forward-looking statements. All forward-looking statements speak only as of the date such statements are made, and neither Blockchain Capital nor the author assumes any duty to update such statements except as required by law. To the extent that any documents, presentations or other materials produced, published or otherwise distributed by Blockchain Capital are referenced in any blog post, such materials should be read with careful attention to any disclaimers provided therein.

.png)

.png)

.png)

No Results Found.