.jpg)

Lessons from the Cloud

Capital follows the path of least resistance – and stays where efficiency compounds.

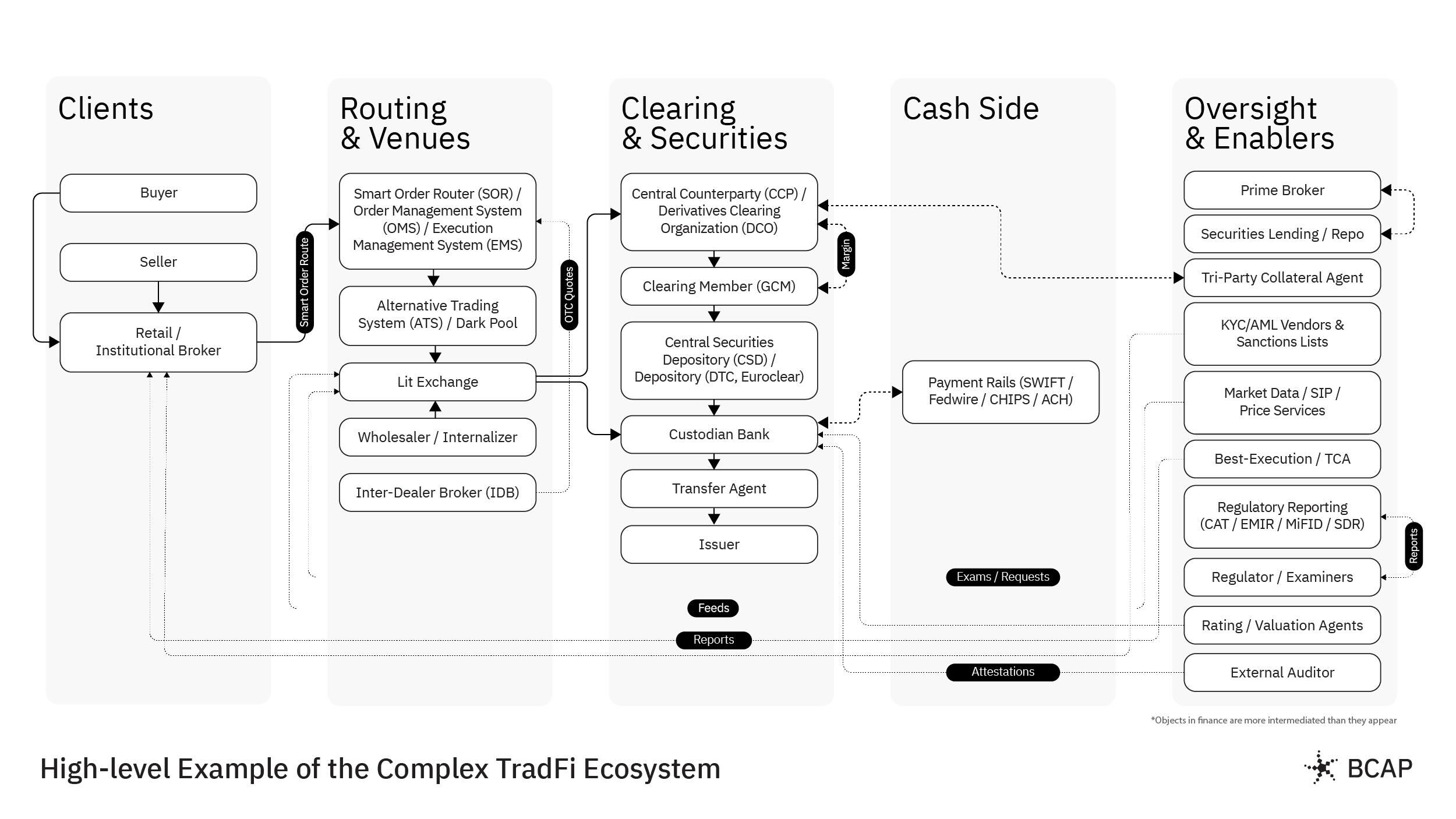

If you feel like money already works, you’re not wrong. Tap, pay, and your balances update. It looks efficient. Until you peek below the surface.

Behind every financial transaction there is a costly relay through the private books of banks, brokerages, and transfer agents. The result is a delicately choreographed, post-transaction reconciliation across opaque counterparties – a Rube Goldberg machine of regulatory complexity and compliance.

“Don’t get fired” takes precedence over “find alpha” as companies burn billions just to answer one simple question: who owns what?

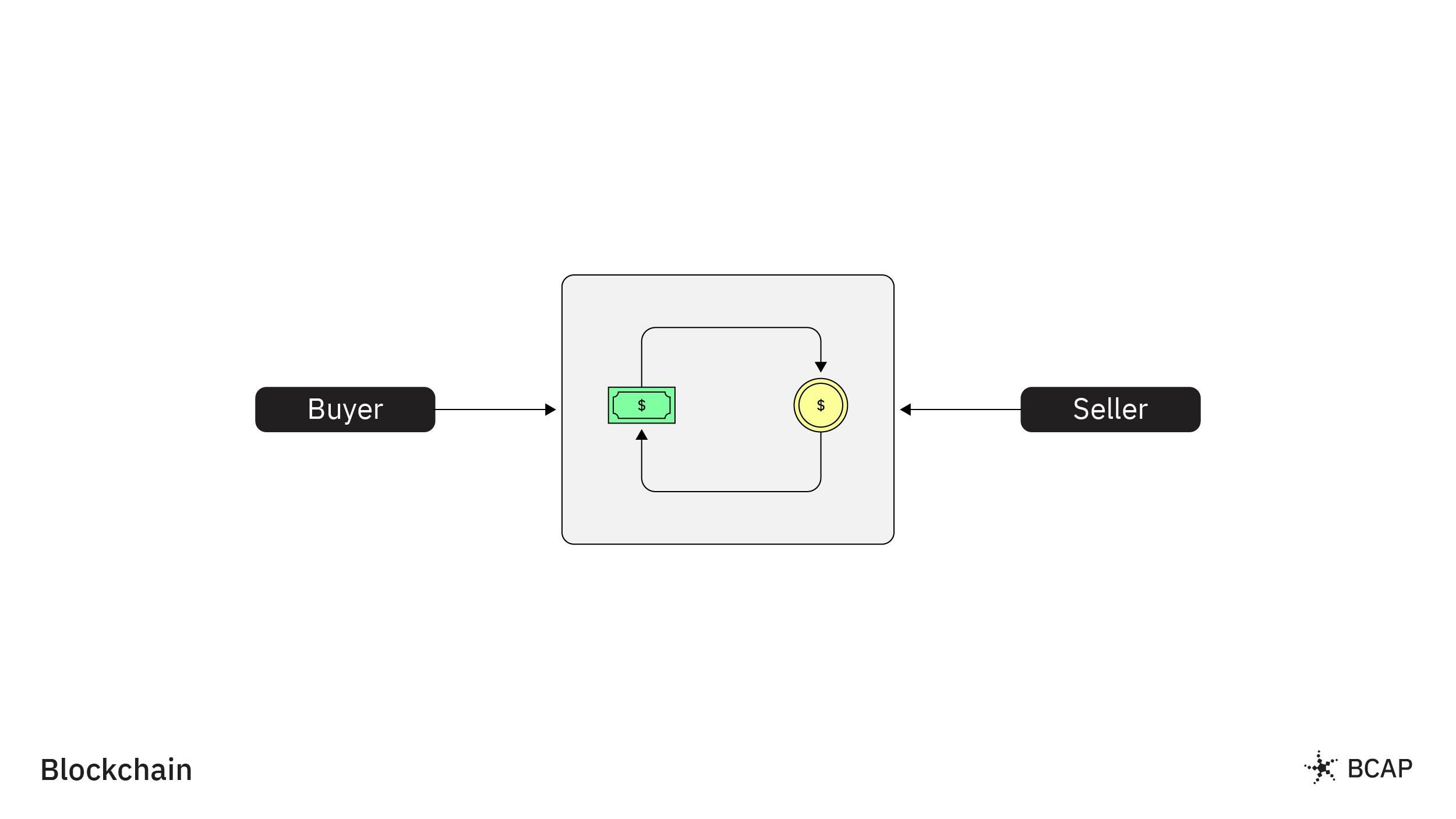

Blockchains dismantle these barriers by turning my record and your record into the record. Onchain transactions settle atomically – like a swap, so assets and cash move together, or not at all.

Once shared rails replace custom plumbing, everything tends to get cheaper, faster, and more reliable.

We’ve seen this before: pre-cloud, front ends worked but every company ran its own brittle, expensive back ends. Once shared infrastructure emerged, innovation flourished. It’s an arc worth revisiting.

It’s hard to believe, but until the 1990s the U.S. classified strong encryption as a munition, right alongside missiles and tanks.

Netscape’s SSL, enabling secure online credit-card payments, arrived in 1995 but adoption stalled until U.S. regulations eased, setting the framework for global e-commerce adoption (a blueprint for today, where innovation leads and regulation follows).

With restrictions lifted, enterprises pushed customer journeys online. But without trusted infrastructure, the safe move was to own the stack end-to-end. Everyone rebuilt the same plumbing in parallel, over investing in redundant capacity provisioned for peak loads (e.g., Black Friday).

This redundancy was individually rational but collectively inefficient. And it persisted until a credible alternative coordinated the market.

That turning point came in 2006, when Andy Jassy announced Amazon Web Services (AWS). AWS flipped the model from siloed back ends to a shared, elastic, always-on, fully redundant, API-first infrastructure you rent, not own.

Economies of scale lowered costs and reduced barriers to entry, sparking a new class of cloud-native breakouts – Airbnb, Netflix, Instagram, Twitter, Slack, Zoom, Stripe, Square, etc.

The cloud crushed costs by centralizing infrastructure and achieving economies of scale. But for all of its benefits, the cloud’s convenience eventually morphed into competitive moats.

As power centralized, take rates rose, APIs and defaults gated reach, and terms shifted unilaterally. For the user, this showed up as rate limits, downranking, or deplatforming.

Blockchains, in turn, can reduce settlement costs by standardizing rules and decentralizing control, fostering open, credibly neutral infrastructure. With no gatekeepers to dictate terms, users gain freedom from arbitrary limits or ad hoc rule changes.

Nevertheless, the cloud showed that shared platforms and de-facto standards often outperform proprietary back ends. That same pattern is repeating. This time, it’s dollars, not data.

Today, the total stablecoin market exceeds $300B with daily on-chain transaction volumes often surpassing $1B, putting stablecoin liquidity and usage on par with Visa and Mastercard.

The benefits show up in the real economy, not just in whitepapers.

In Lagos, merchants use platforms like Yellow Card to move USDT across borders in minutes, not days, bypassing correspondent banks, FX markups, and wire fees. A business owner who once waited a week and lost 8.4% to intermediaries now settles instantly at near-zero cost.

Capital is finding the path of least resistance.

If Yellow Card is the demand signal, Tether is the supply-side. Holding nearly 60% market share and over $175B circulating supply, Tether earns like a bank (think insurance float without underwriting risks), scales like SaaS, and distributes like an API.

And just as Google turned attention into cashflow by monetizing internet traffic, Tether can run the same playbook with USDT (and now USA₮). As the settlement unit for onchain commerce, Tether earns interest on the assets backing its reserves (mostly U.S. T-Bills). In 2024, Tether’s net profit exceeded $13B.

Tether’s moats are distribution and liquidity. Embedded at the endpoints where money actually moves, Tether is positioned to stack services (payments, FX, merchant acquiring, payroll, credit, etc) as it signals a move from product to platform.

Make settlement cheap and everywhere, and the next primitive is borrow/lend. Enter Aave: a global, 24/7, over-collateralized repo market run by code. Lenders park USDT in a common pool, borrowers draw against it at floating rates set by supply/demand, and collateral is marked-to-market and auto-liquidated.

Since inception in 2017, Aave has successfully processed billions in loans while generating nearly $300M in revenue.

By treating credit as software, Aave’s liquidity pools price risk in code, settle instantly, and run without borders or banking hours.

When risk is priced by math and collateral is natively verifiable, credit stops being a favor and becomes a public good. No gatekeepers and no one saying “You must be this tall to ride.”

Reducing barriers to the flow of capital triggers a profound restructuring of economic systems and the markets that drive them.

Polymarket carries this pattern forward by turning opinions into a tradable probability, operating as a global, always-on marketplace that settles instantly in stablecoins. If you think the market is wrong, take the other side and buy $1 at a discount. Put your money where your mouth is.

Polymarket’s trading volume surged to roughly $9B in 2024 and is now clearing +$1B monthly in 2025. With ICE’s $2B strategic investment and data-distribution deal, Polymarket’s event probabilities will likely show up in Bloomberg terminals and ICE feeds. Traders, analysts, and risk desks will be able to treat prediction markets like any other market-implied probability — alongside options, futures, and rates data.

That potential visibility collapses the distance between on-chain sentiment and institutional decision-making.

We’ve moved from proof of concept to proof of business – Yellow Card, Tether, Aave, Polymarket, etc – with real volumes, real cash flows, and real users.

Just as U.S. regulatory policy normalized strong encryption, easing regulatory regimes alongside new legislation like the GENIUS Act opens new pathways for onchain finance. Innovation leads, policy follows. Again, the trajectory rhymes.

As money moves like data, finance becomes composable. Here’s how this might unfold:

- Stablecoins become the default cross-border medium. Dollars follow the path of least resistance, especially for SMEs and marketplaces. Onchain dollar balances compound from $300B today to potentially $4T by 2030 as better, faster, cheaper wins.

- The ledger moves from private to public, and funding rates reprice. As dollars exit bank ledgers for programmable stablecoins, bank balance sheets shrink, pushing the cost of capital and user fees higher. Banking woes deepen as onchain liquidity compounds.

- Tokenization unlocks new frontiers. As capital accumulates onchain, it draws in global liquidity, developers, and tokenized assets. Tokenization won’t make bad assets good, but it will make good ones liquid, accessible, and interoperable.

- Liquidity evolves into software. When cash and assets move together with T+0 settlement, instant margining, and programmable waterfalls, the velocity of capital accelerates. Collateral turns over faster, operational risk premia shrink, and spreads compress alongside friction.

Ultimately, as dollars leave bank ledgers for programmable money, banks lose their grip on cheap funding as float and credit migrates to tokenized markets. When financial primitives run within the applications people already use, liquidity evolves into software.

Financial rails are standardizing, liquidity is pooling, and policy is widening the opportunity set. When transactions and settlement happen instantly, and money functions like code, markets don’t just get cheaper and faster, they will likely get wider, weirder, and more programmable (e.g., “the internet of value”).

As with any wave of innovation, many experiments will fail. The ones that succeed will redraw our financial landscape.

An affiliate of Blockchain Capital may be an investor in one or more of the protocols or companies mentioned above. The views expressed in each blog post may be the personal views of each author and do not necessarily reflect the views of Blockchain Capital and its affiliates. Neither Blockchain Capital nor the author guarantees the accuracy, adequacy or completeness of information provided in each blog post. No representation or warranty, express or implied, is made or given by or on behalf of Blockchain Capital, the author or any other person as to the accuracy and completeness or fairness of the information contained in any blog post and no responsibility or liability is accepted for any such information. Nothing contained in each blog post constitutes investment, regulatory, legal, compliance or tax or other advice nor is it to be relied on in making an investment decision. Blog posts should not be viewed as current or past recommendations or solicitations of an offer to buy or sell any securities or to adopt any investment strategy. The blog posts may contain projections or other forward-looking statements, which are based on beliefs, assumptions and expectations that may change as a result of many possible events or factors. If a change occurs, actual results may vary materially from those expressed in the forward-looking statements. All forward-looking statements speak only as of the date such statements are made, and neither Blockchain Capital nor each author assumes any duty to update such statements except as required by law. To the extent that any documents, presentations or other materials produced, published or otherwise distributed by Blockchain Capital are referenced in any blog post, such materials should be read with careful attention to any disclaimers provided therein.

.png)

.png)

.png)

No Results Found.